The Federal Reserve plays a central role in financial markets and the economy, and its importance has only grown in recent decades. From the 2008 global financial crisis to the inflationary period of the past several years, investors have followed every Fed decision carefully. So, when leadership changes occur at the Fed, they naturally capture the attention of investors and the broader public. At the same time, it’s important to understand what the Fed does and does not control when it comes to long-term investing.

The new Fed Chair confirmed by the Senate is Kevin Warsh, an experienced policymaker who served on the Fed’s Board of Governors during the global financial crisis.1 Markets have generally responded favorably to Warsh’s nomination, viewing him as a known quantity with familiarity with the Fed and monetary policy. What might this mean for Fed policy and investor portfolios in the coming years?

The economy has grown under many Fed leaders

Fed leadership transitions are infrequent, so it’s helpful to zoom out for perspective. The Chair of the Federal Reserve is nominated for a 4-year term, while members of the Board of Governors serve 14-year rotating terms. The primary reason for this structure is to separate monetary, regulatory, and supervisory decisions from politics. This is often referred to as “Fed independence,” a concept that has been tested and debated across history.

The accompanying chart shows that the U.S. economy has grown across the tenures of different Fed chairs, regardless of which president nominated them. Paul Volcker, Alan Greenspan, Ben Bernanke, Janet Yellen, and Jerome Powell each navigated unique economic challenges, from stagflation in the 1970s and early 1980s to the global financial crisis, the pandemic, and the recent inflation surge. In between, there have been numerous market and economic cycles that forced the Fed to react to new circumstances, in some cases by using its policy tools in new ways.

The Fed and interest rates are only one part of the equation when it comes to the health of the economy. The Federal Reserve Reform Act of 1977 established a “dual mandate” to promote maximum employment and stable inflation, which, ideally, should result in predictable long-term borrowing costs for consumers, businesses, and the government.

However, despite how the market often views the Fed, the central bank does not control all aspects of the economy. Many of their tools, such as the federal funds rate, are often viewed as blunt instruments that work with what economists refer to as “long and variable lags.” Economic shocks, technological change, demographics, and global events all play significant roles. For instance, the Fed can react to rising gasoline prices and the impact of AI on the job market, but it cannot control them directly.

What this means for investors is that while the Fed plays an important role, and interest rates do influence many parts of the economy and financial markets, focusing too much on each Fed decision can result in missing the forest for the trees. Instead, understanding the underlying market and economic drivers that the Fed is navigating can help investors maintain a long-term perspective.

Kevin Warsh believes in a more focused Fed

Like all government institutions, the Fed is imperfect and does not have a crystal ball as to where the economy might go next. Instead, when making their decisions, they use the same public and private economic data that all economists rely on. So, it’s natural that there are often criticisms of the Fed in terms of specific policy decisions and as an institution. As with all aspects of investing, it’s often important to set politics aside to better distinguish what the Fed might do from what we believe they ought to do.

In his recent Senate testimony, Warsh stated that he favors “a clearer, cleaner match between the Fed’s powers and responsibilities,” suggesting a preference for a more focused central bank.2 He also emphasized that “monetary policy independence is essential” and that policymakers must act in the nation’s interest. In the past, Warsh was seen as an “inflation hawk,” meaning that his policy preference would be to err on the side of higher interest rates to prevent inflation from rising, as well as promoting reform at the Fed.

When it comes to investing, there are at least three implications based on his views. First, it will take time to fully understand how Warsh’s current views will affect policy in this inflationary environment, especially if they conflict with the White House’s preference for lower rates. He may need to address this as soon as his first press conference, since high oil prices will weigh on upcoming Fed decisions.

That said, this would not be the first time there has been a conflict between the executive branch and the Fed, since elected officials naturally prefer lower interest rates to boost the economy. Famously, conflicts arose between President Lyndon B. Johnson and Fed Chair William McChesney Martin Jr., between Ronald Reagan and Paul Volcker, and, most recently, between Donald Trump and Jerome Powell, and more. This has occurred even when the Fed Chair is appointed by the president.

Inflation and the money supply complicate Fed decision-making

Second, while Warsh believes the Fed has overstepped with its green initiatives and social policies, he has not argued for wholesale changes to the institution’s core. Specifically, Warsh believes that crisis-era actions such as the expansion of the Fed’s balance sheet were appropriate, since, after all, he was in the room when many of those decisions were made.3

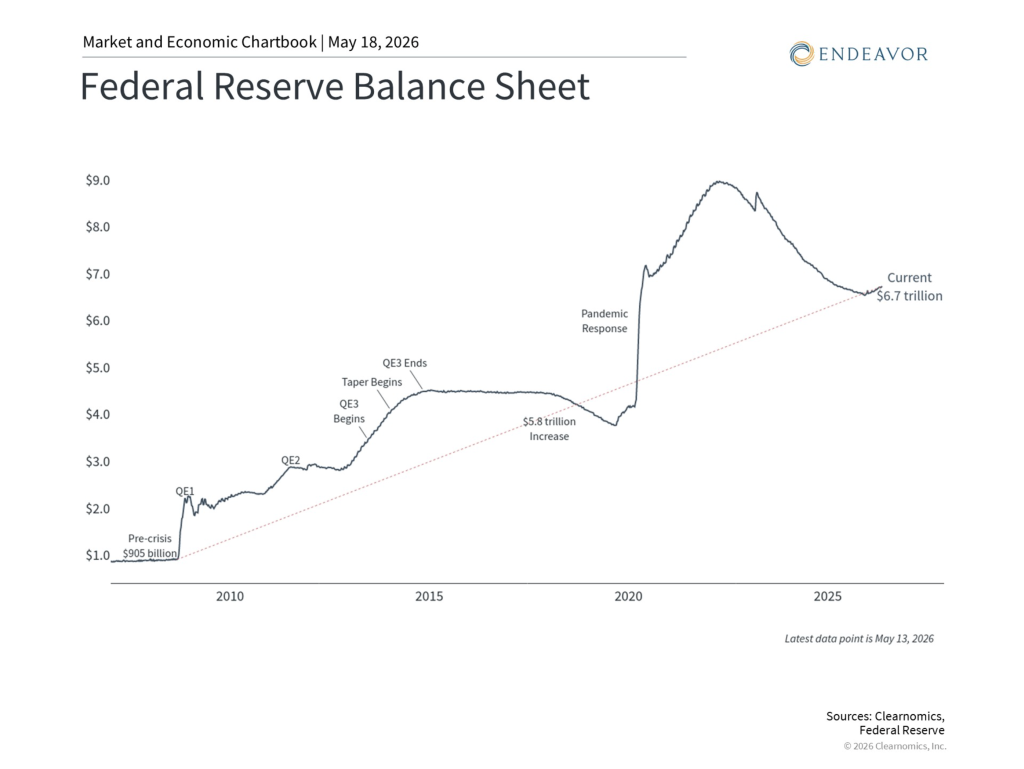

Instead, he believes the Fed should “retrace its steps” once conditions normalize and the crisis is over. In other words, the Fed’s balance sheet, which remains sizable at $6.7 trillion, is not where it ought to be now that the 2008 financial crisis and the pandemic are long over. In theory, shrinking the balance sheet should tighten financial conditions, since this involves either selling or reinvesting less each month in Treasury securities and mortgage-backed securities. This is often known as “quantitative tightening,” the opposite of the easing done during crisis periods. Changes in this policy can affect bond prices, mortgage rates, and corporate borrowing costs.

Third, Warsh believes that Fed policy, especially since the pandemic, has contributed to the growth of the federal deficit and national debt. Just as with the Fed’s balance sheet, he argues that while spending may be justified in recessions, it should be symmetric and monetary policymakers should steer clear of fiscal commentary.4

Of course, the Fed does not directly control federal spending, and it’s unclear what the new Fed Chair would do differently to influence budgets passed by Congress. To the extent the Fed does weigh in on the size of the budget deficit, it would either provide guidance or control interest rates. For investors, this is another reason that policy rates may continue to depend on many factors in the coming years.

The new Fed Chair inherits a particularly challenging economic environment. Inflation has accelerated in recent months due to higher oil and gasoline prices, driven by the war in Iran. Headline CPI was 3.8% year-over-year as of April 2026, with core CPI at 2.8%, both still above the Fed’s 2% target.

This has created a difficult policy backdrop. While many at the Fed and in markets had previously been expecting further rate cuts, fed funds futures now reflect the possibility that the Fed may need to consider a rate increase by early 2027. These market expectations should be taken with a grain of salt, as they shift frequently in response to new economic data and global events. Still, they highlight the uncertain path ahead for monetary policy.

For investors, the most important takeaway is that markets and the economy have performed well across many different Fed leadership transitions and policy environments. Changes at the top of the Fed naturally generate uncertainty, but they rarely alter the long-term fundamentals that drive financial markets. Earnings growth, productivity, demographics, and innovation are ultimately the most important drivers of long-run returns.

The bottom line? As Kevin Warsh takes over as Fed Chair, it’s important to maintain perspective on the role of the Fed. Ultimately, understanding the longer-term drivers of the market and economy is the best way to achieve financial goals.

Endeavor Advisors, LLC (“Endeavor”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Endeavor and its representatives are properly licensed or exempt from licensure.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance, and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

The information provided is for educational and informational purposes only and does not constitute investment advice, and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. You should consult your attorney or tax advisor.

Diversification does not ensure a profit or guarantee against loss.

Investing in commodities entails significant risk and is not appropriate for all investors.